Use this file to discover all available pages before exploring further.

View on GitHub

Open this notebook in GitHub to run it yourself

Portfolio optimization [1] is the process of optimally allocating a portfolio of financial assets, according to some predetermined goal. Usually, the goal is to maximize the potential return while minimizing the financial risk of the portfolio.One can express this problem as a combinatorial optimization problem like many other real-world problems.This demo shows how to employ the Quantum Approximate Optimization Algorithm (QAOA) [2] on the Classiq platform to solve the problem of portfolio optimization.

First, model the problem mathematically using a simple yet powerful model that captures the essence of portfolio optimization:

A portfolio is built from a pool of n financial assets, with each asset labeled i∈{1,…,n}.

Every asset’s return is a random variable, with expected value μi and variance Σi (modeling the financial risk involved in the asset).

Every two assets i=j have covariance Σij (modeling market correlation between assets).

Every asset i has a weight wi∈Di={0,…,bi} in the portfolio, with bi defined as the budget for asset i (modeling the maximum allowed weight of the asset).

The return vector μ, the covariance matrix Σ, and the weight vector w are defined naturally from the above (with the domain D=D1×D2×…×Dn for w).

With the above definitions, the total expected return of the portfolio is μTw and the total risk is wTΣw.Use a simple difference of the two as the cost function, with the additional constraint that the total sum of assets does not exceed a predefined budget B.Note that there are many other possibilities for defining a cost function (such as adding a scaling factor to the risk/return or even a non-linear relation).For simplicity, select the model below and assume all constants and variables are dimensionless.

Thus, given the constant inputs μ,Σ,D,B, the problem is to find the optimal variable w:w∈DminwTΣw−μTw,subject to Σiwi≤B.This case is called integer portfolio optimization, since the domains Di are over the (positive) integers.Another variation of this problem defines weights over binary domains, and is not discussed here.

To solve the Pyomo model defined above, use the CombinatorialProblem Python class.Under the hood, it translates the Pyomo model to a quantum model of the QAOA algorithm, with the cost Hamiltonian translated from the Pyomo model.Choose the number of layers for the QAOA ansatz using the num_layers argument and the penalty_factor, which is the coefficient of the constraints term in the cost Hamiltonian:

from classiq.execution import *execution_preferences = ExecutionPreferences( backend_preferences=ClassiqBackendPreferences(backend_name="simulator"),)

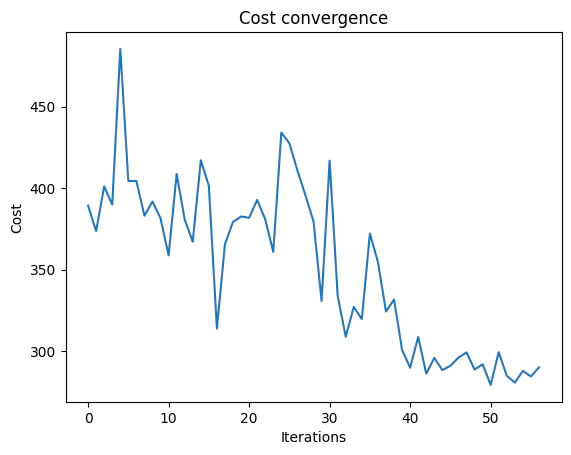

Solve the problem by calling the optimize method of the CombinatorialProblem object.For the classical optimization part of the QAOA algorithm, define the maximum number of classical iterations (maxiter) and the α-parameter (quantile) for running CVaR-QAOA, an improved variation of the QAOA algorithm [3]:

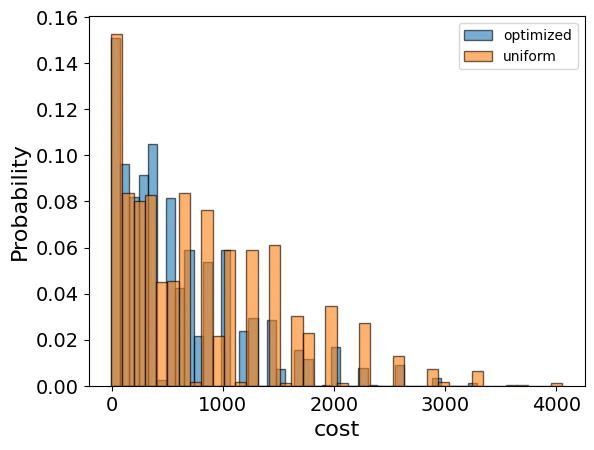

Examine the statistics of the algorithm.The optimization is always defined as a minimization problem, so the positive maximization objective is translated to negative minimization by the Pyomo-to-Qmod translator.To get samples with the optimized parameters, call the sample method:

Lastly, compare with the classical solution of the problem:

from pyomo.opt import SolverFactorysolver = SolverFactory("couenne")solver.solve(portfolio_model)portfolio_model.display()classical_solution = [ round(pyo.value(portfolio_model.w[i])) for i in range(len(portfolio_model.w))]print("Classical solution:", classical_solution)

Most of the solutions obtained by running QAOA are close to the minimal solution obtained classically, demonstrating the effectiveness of the algorithm. Also, note the non-trivial solution, which includes a non-zero weight for the asset with negative expected return, demonstrating that it sometimes makes sense to include such assets in the portfolio as a risk-mitigation strategy - especially if they are highly anti-correlated with the rest of the assets.