View on GitHub

Open this notebook in GitHub to run it yourself

Building a Geometric Brownian Motion (GBM) Price Model — from Analytic Formula to Quantum Circuit

Motivation

Pricing path-dependent derivatives such as Asian options often requires evaluating a Geometric Brownian Motion (GBM) over many time steps.- Classical approach: Monte Carlo simulation over many paths and timesteps.

- Quantum approach:

- Compress the representation of randomness (load distributions into amplitudes).

- Achieve a quadratic speed-up for expectation estimation via Quantum Amplitude Estimation (QAE).

- Derive a Chebyshev-truncated Karhunen–Loève (KL) expansion.

- Convert that expansion to Classiq quantum arithmetic.

- Synthesize hardware-aware circuits for multiple targets with a single command.

- Chebyshev Polynomials in the KL Expansion

KL expansion (Chebyshev-truncated form)

The KL expansion expresses as an orthogonal sine series with i.i.d. Gaussian coefficients . In truncated form: where are Chebyshev polynomials of the second kind.Gaussian discretization (classical preprocessing)

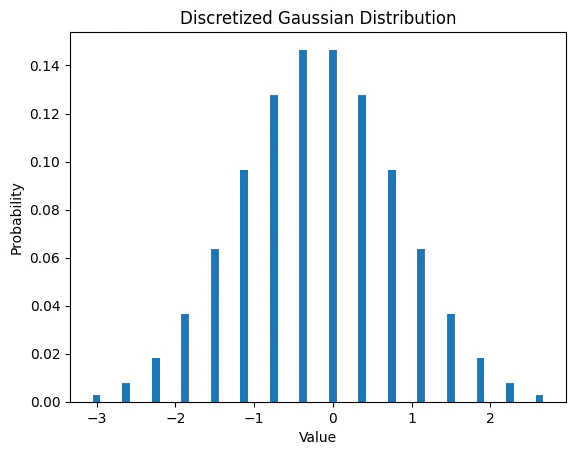

Goal: build a discrete approximation of a Gaussian distribution so that its probabilities can be loaded into amplitudes. Typical steps:- Select range (e.g., standard deviations).

- Use bins for qubits.

- Compute bin probabilities using the Gaussian CDF:

- Normalize the probability vector so .

- A list of grid points (bin edges or centers)

- A probability vector suitable for amplitude loading.

Quantum function approximation for and

For simplicity in the demo:- Implement and via low-order Taylor-like polynomials (around ).

- This keeps the arithmetic shallow and highlights the modeling flow.

- After preparing a superposition over , the computed value register becomes entangled with , representing a function evaluation “in parallel worlds.”

Output:

Output:

Output:

Chebyshev Polynomials

The Chebyshev polynomials are a sequence of orthogonal polynomials that are related to de Moivre’s formula and the trigonometric functions. They are defined by the recurrence relation:- Loop depth grows as .

- Doubling truncation order increases gate count only linearly (hardware-friendly).

Output:

Output:

Brownian Motion

The Brownian motion is a stochastic process that models the random movement of particles in a fluid. The approximate solution in this context is the truncated Wiener series. Key ingredients in the quantum model:- Prepare registers for coefficients (a_0,\dots,a_{L-1}) from the discretized Gaussian distribution (amplitude loading).

- Prepare a time register (t) in superposition (e.g., Hadamards over a time index).

- Compute:

- (or a stand-in approximation)

- (or a stand-in approximation)

- via recurrence

- Accumulate the weighted sum to form .

Return-to-price space (GBM mapping)

Convert (log-)returns to price using the GBM form: In the demo notebook :- Exponentiation may be implemented via a simple approximation for .

- More accurate quantum exponentiation methods exist in the literature (see referenced suggestions in https://arxiv.org/pdf/2001.00807.pdf for example).

Putting it all together

Output:

Output:

Output:

Final reflection and quantum roadmap

This notebook illustrates that a mathematically heavy model (KL-truncated GBM + Chebyshev recursion) becomes circuit-light once randomness is moved into amplitudes. Next steps toward pricing (expected payoff):- Amplitude loading: put Gaussian coefficients into superposition with gates (matching the power-of-two grid).

- Nested QAE (conceptually):

- First QAE estimates time-averaged price along the path.

- Second QAE wraps the payoff.

- Query complexity can still beat classical Monte Carlo scaling.

- Potential shortcut (as hinted in the reference):

- Drop one QAE via smart time subsampling to reduce depth without extra qubits (constants and practical tradeoffs depend on implementation details).

- The classical formula is algebraically dense, but the quantum program is highly structured, enabling modeling-focused development with automated circuit synthesis.